Balance Sheet and Hedging Trends Since the Pandemic: Depository Member Snapshot

by Raj Sisodia, Managing Director, Member Credit & Quantitative Strategies

The introduction of direct fiscal transfers and accommodative monetary policies resulted in broad-based depository member balance sheet transformations, following the onset of the global pandemic.

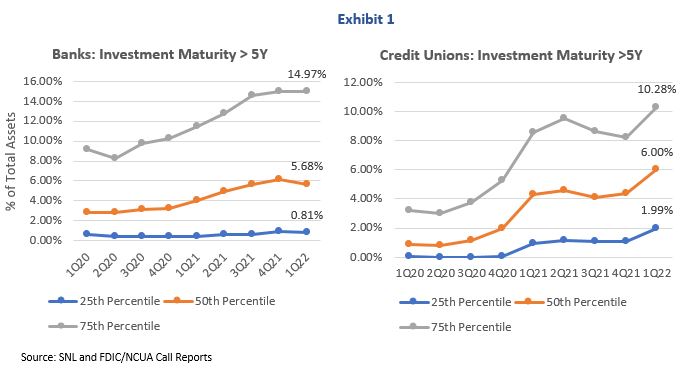

Stimulus checks resulted in the paydown of consumer loans while $4.8 trillion in Fed’s open market purchases made its way to deposits at depository member institutions. The combination of loan paydowns and deposit increases led to higher levels of cash balances and lower yielding investment securities. Many depository members opted to defend against severe margin compression by going further out on the interest rate curve over the past two years. (Exhibit 1)

The trend towards longer duration assets is significantly more pronounced for credit union members as most credit unions had previously viewed investment portfolios as a source of liquidity rather than a source of yield. Given the difficulty in generating loans in an environment where consumers are flush with cash, the median credit union member experienced a growth multiplier of six times in the long duration investment book over the past two years (compared to the median bank member that saw a two times increase over the same period).

Hedging Trends

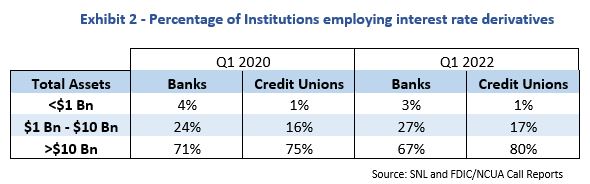

Despite rising inflation and interest rates being at the forefront of the news cycle over the past year, there has been minimal change in hedging behavior among depository members (Exhibit 2). Large bank and credit union members (>$1 billion in assets) employ derivatives to hedge interest rate risk whereas community bank and smaller credit union members (<$1 billion in assets) partially mitigate their interest risk through portfolio concentration limits of fixed rate assets. The noticeable difference between derivatives use amongst large institutions and community institutions may be explained by the level of asset-liability management sophistication demanded by regulators given the likely correlation between more complex loans and the size of the financial institution. Larger depository members also tend to have more resources at their disposal to employ more robust asset-liability tools or vendor software

Impact of Rising Rates on Investment Portfolio

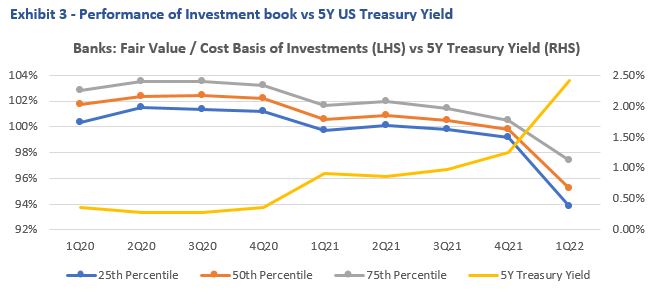

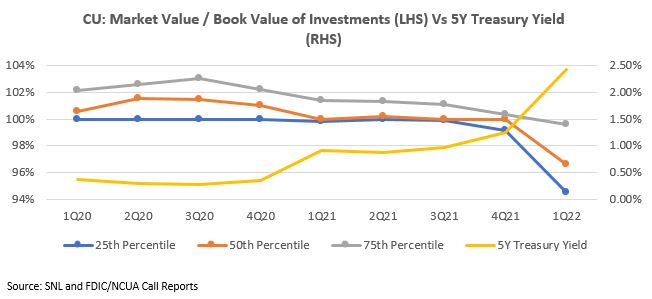

Interest rate decline at the start of the pandemic and the subsequent rebound led to fluctuations in the market value of depository members’ investment portfolio. Sharp increase in the 5-year U.S. Treasury yield from 1.26% to 2.42% during 1Q 2022 resulted in significant valuation losses in the investment book (Exhibit 3). Both bank and credit union members faced a sharper decline, with some banks facing larger decline compared with the median decline trend, due to larger amounts of MBS holdings, which are more sensitive to interest rate increases.

Looking Forward

With the 5-year treasury yield moving up another 90 bps since the end of 1Q 2022, depository members will continue to see noticeable earnings headwind/unrealized losses into 2Q. With the sharp rise in frontend rates, reversal of liquidity flow in the economy, and increasingly attractive loan yields, the size of the long duration investment book has likely peaked for depository members. Although the investment book is a source of earnings drag for the near term, the risk remains manageable given solid capital buffers built up during the pandemic, which will support a moderate level of earnings volatility for the duration of the cycle.

Disclaimer: The information contained in this paper is for informational purposes only and should not be construed as a solicitation or offer or advice (financial, legal or otherwise) by the Bank. Cited information is derived from sources generally believed by the Bank to be reliable, but the Bank does not warrant the accuracy or reasonableness of the information or of any assumptions or other information contained in this paper, and the Bank expressly disclaims responsibility for any errors or omissions in computing or disseminating the information, and any use to which the information is put. The Bank further expressly disclaims any obligation to update the information presented in this paper.